Inflation remains hot, and the Federal Reserve pushes forward on its mission to tame inflation. With the most recent 75-basis-point increase in the key overnight rate, the Federal Reserve brought the benchmark rate to the 2.25%-2.50% range. Unfortunately, on the heels of this rate hike, GDP declined 0.9% second quarter and 1.3% through the first half of 2022. Adding to the reported GDP levels, recent earnings reports and guidance from Best Buy, Walmart, Target, and other retailers are guiding toward lower expectations for the remainder of 2022. While the above data may not be the textbook definition of an economic recession, it is widely “felt” that we are indeed in one.

What does all this mean for credit unions?

Credit unions should consider several factors when evaluating the current economic backdrop. First, we have no certainty the most recent rate hike will be successful in bringing inflation under control. In fact, Federal Reserve Chair Jerome Powell suggested there may be a few more rate hikes in 2022, bringing the likely peak Fed Funds rate to a range of 3.25-3.50%. The Federal Reserve believes the current 2.25-2.50% range is the neutral Fed Funds rate (a rate that is neither restrictive nor accommodative.) This means the Federal Reserve intends to move the Fed Funds rate into a restrictive stance, even though the economy is likely already in a recession.

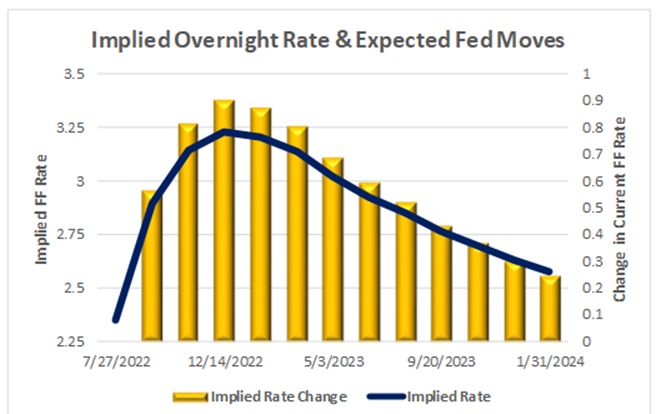

Considering the above, it would be fair to assume the Federal Reserve will continue to increase rates through the remainder of 2022. However, the graph below illustrates the general market is expecting the Fed Funds target rate to peak in December 2022 and to start declining in the first quarter of 2023.

Source: Bloomberg

This means credit unions are beginning to see the light at the end of the tunnel. Short-term rate increases should come to an end within the next few months, but the market then anticipates an immediate turn to rate cuts.

How should credit unions navigate this rapidly evolving environment?

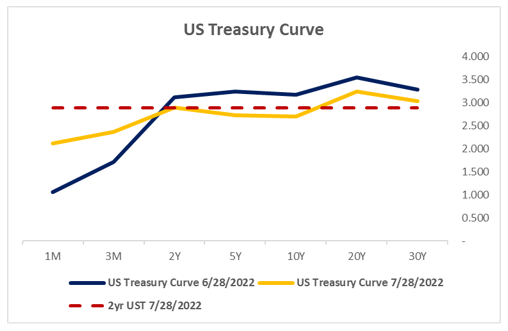

First, consider that interest rates are likely near their peak. This is highlighted by the recent declines in the 10-year U.S. Treasury rate and the overall flatness of the yield curve. If interest rates are near their peak, it may be time to consider adding duration (maturity) to your balance sheet. The chart below shows the 48 basis point decline in the 10 year U.S. Treasury over the last month. An inversion of 19 basis points occurs between the 2-year and the 10 year Treasury curve.

From a management or strategy perspective, credit unions could benefit from locking in yield and duration to support net interest income in the future. However, with mortgage volume slowing because of the significant increases in mortgage rates, executing this strategy is becoming more difficult. Further, most credit unions are under heavy pressure with high to extreme measures on their NEV Supervisory Tests. But, mortgage volume is not the only option for adding duration. Credit unions can also consider opportunities within the securities markets and commercial lending. However, if we are in the early stages of a recession, tighter underwriting criteria becomes more important.

On the deposit side, many credit unions are seeking strategies to return value to their membership. This often requires credit unions to choose between raising non-maturity deposits and offering term deposit specials. The relative impact of an increase in non-maturity deposit rates can be significant, as the entire balance reprices higher immediately. With the prospect of a recession and potential for increased credit losses in the future, credit unions are encouraged to protect their margins and maintain sound capital growth. As a result, consider offering term deposit specials that can be matched off against a “like-term” investment alternative for a healthy spread. Many such opportunities exist along the yield curve that can provide value to your membership without jeopardizing the safety of your credit union.

If you decide an increase in non-maturity deposits is the best path, consider making increases in dividend rates commensurate with increases in average loan rates. “Pegging” dividend rate increases to loan yield increases helps absorb the bulk of interest expense increases through interest income, which helps maintain and protect your margin.

In summary, we are nearing an inflection point in the economy, where we transition from a rising rate to a falling rate environment. Credit unions should begin adjusting their strategies and repositioning their asset allocation to support a wider net interest margin. This will help build net worth as interest rates begin to move back down. Yes, there is pressure to raise dividend rates. However, this can be accomplished strategically in a way that provides value to your membership without eroding net worth contributions. On the asset side, it is time to find ways to add duration (maturity) to the balance sheet and lock in attractive market rates; they probably will not be around for long.

Please contact Rachelle Wegner, with MemberClose, at 720.823.8110 or rwegner@MemberClose.com for more information.